What This Guide Covers

The Indian real estate market continues to attract interest from Non-Resident Indians (NRIs), whether as long-term investors or former residents holding ancestral property. But when it comes to selling or renting out property in India, NRIs often find themselves entangled in complex legal rules, tax obligations, and banking formalities.

This blog is a simplified, updated guide that answers the most crucial questions:

-

Can NRIs legally sell residential or commercial property in India?

-

Are there restrictions on renting it out to tenants?

-

What about taxes, FEMA regulations, or repatriating the money earned abroad?

We’ll break down what the law says—especially under the Foreign Exchange Management Act (FEMA) and relevant income tax rules—to help you avoid common pitfalls.

Whether you’re an NRI planning to sell a flat in Delhi, rent out a commercial unit in Bangalore, or transfer sale proceeds abroad, this blog will help you understand your rights and responsibilities. Plus, we’ll provide expert tips and checklists to make sure your transaction is compliant and hassle-free.

So, if you’re unsure about the legalities of managing your Indian property from overseas, you’re in the right place.

What Types of Properties Can NRIs Sell or Rent Out?

NRIs enjoy similar property rights in India as resident Indians—with a few notable restrictions. The type of property you hold plays a crucial role in determining whether you can sell or lease it legally.

Properties NRIs Can Freely Sell or Rent:

-

Residential Property

-

You can sell your apartment, flat, bungalow, or house to an Indian resident, another NRI, or a Person of Indian Origin (PIO).

-

You can also rent it out without restriction—either long-term lease or short stays—subject to income tax compliance.

-

-

Commercial Property

-

Office spaces, shops, warehouses, and commercial plots can be sold or leased without any legal hurdle to Indian residents, NRIs, or PIOs.

-

Rental income from these is fully allowed under FEMA rules.

-

Property NRIs Cannot Sell or Buy:

-

Agricultural Land, Plantation Property, and Farmhouses

-

NRIs cannot purchase such land, even if they inherit it.

-

While you may inherit agricultural property, you cannot sell it to another NRI or PIO—only to an Indian citizen who is a resident.

-

Important Notes:

-

If the property is jointly held with a resident Indian or inherited through a will, additional documentation may be required during the sale process.

-

Always ensure clear title, mutation, and registration records before initiating sale or rent, especially if the property has been unoccupied for years.

Understanding the category of your property is the first step in navigating the legal landscape confidently. The next section will explain how FEMA governs the sale and rental process for NRIs in India.

Legal Rights Under FEMA (Foreign Exchange Management Act)

For NRIs, property transactions in India—especially selling or renting—are governed by the Foreign Exchange Management Act (FEMA). This law ensures all cross-border dealings are tracked and compliant with India’s financial regulations.

What FEMA Allows NRIs to Do:

-

Sell residential or commercial property to:

-

An Indian citizen living in India

-

Another NRI or Person of Indian Origin (PIO)

-

-

Rent out any legally owned residential or commercial property and earn income in India

-

Repatriate sale or rental proceeds overseas, provided certain conditions are met (discussed in later sections)

However, FEMA does not permit NRIs to:

-

Buy or sell agricultural land, plantation property, or farmhouses

-

Sell inherited agricultural property to other NRIs or PIOs (can only sell to Indian residents)

📄 Key FEMA Conditions for Property Sale or Rent:

-

The property must be legally acquired as per FEMA norms—either purchased, inherited, or received via gift.

-

The sale proceeds must be routed through banking channels and can only be credited to the NRO account.

-

Repatriation is allowed up to USD 1 million per financial year, subject to tax compliance.

Selling Property: Step-by-Step Legal Process for NRIs

Selling property in India as an NRI is completely legal—but it must follow a clearly defined process to remain compliant with Indian laws and FEMA regulations. Here’s a step-by-step breakdown to help you avoid delays, rejections, or tax issues.

Step 1: Ensure Clear Legal Title

Before initiating any sale, verify that the title of the property is in your name. If the property is inherited, make sure the mutation, succession certificate (if applicable), and legal heir documentation are complete.

Step 2: Gather All Mandatory Documents

-

PAN Card (mandatory for all property transactions)

-

Sale Deed and earlier title deeds

-

Passport and OCI/PIO Card (if applicable)

-

Proof of address (Indian and overseas)

-

Encumbrance Certificate

-

Tax receipts and utility bill clearance

If a Power of Attorney (PoA) is acting on your behalf, notarized and consular-attested PoA documents must be ready.

Step 3: Find a Buyer

NRIs can sell to:

-

Indian citizens

-

Other NRIs or PIOs (for residential/commercial properties only)

You may list the property through a broker, legal agent, or real estate platform.

Step 4: Draft and Register the Sale Agreement

-

A legal sale agreement is signed detailing the payment terms, handover timeline, and other conditions.

-

The final Sale Deed must be registered at the local sub-registrar office where the property is located.

-

Both buyer and seller (or their PoA holders) must be present with original documents.

Step 5: Receive Payment Legally

-

Funds must be received through Indian banking channels (RTGS/NEFT/cheque).

-

The payment must be credited to your NRO account in India.

Step 6: Pay Capital Gains Tax

If the property is sold after 2 years of holding, Long-Term Capital Gains (LTCG) at 20% with indexation will apply.

-

TDS at 20% is deducted by the buyer (plus surcharge and cess).

-

You may apply for a lower TDS certificate from the Income Tax Department in advance if eligible.

Can NRIs Rent Out Indian Property? (Yes, but Know This)

Yes, NRIs are legally allowed to rent out both residential and commercial property in India—without any special permission from the RBI. Rental income is considered a legitimate source of income for NRIs under Indian law, but it comes with a few legal and tax-related obligations.

What’s Allowed?

-

Types of Properties You Can Rent:

-

Residential apartments, flats, houses

-

Commercial spaces like offices, shops, showrooms

-

-

Who Can Be the Tenant?

-

Indian residents

-

Businesses and companies operating in India

-

You can lease out the property for any duration under a registered rental agreement. Ensure the rental contract complies with the applicable state rental laws.

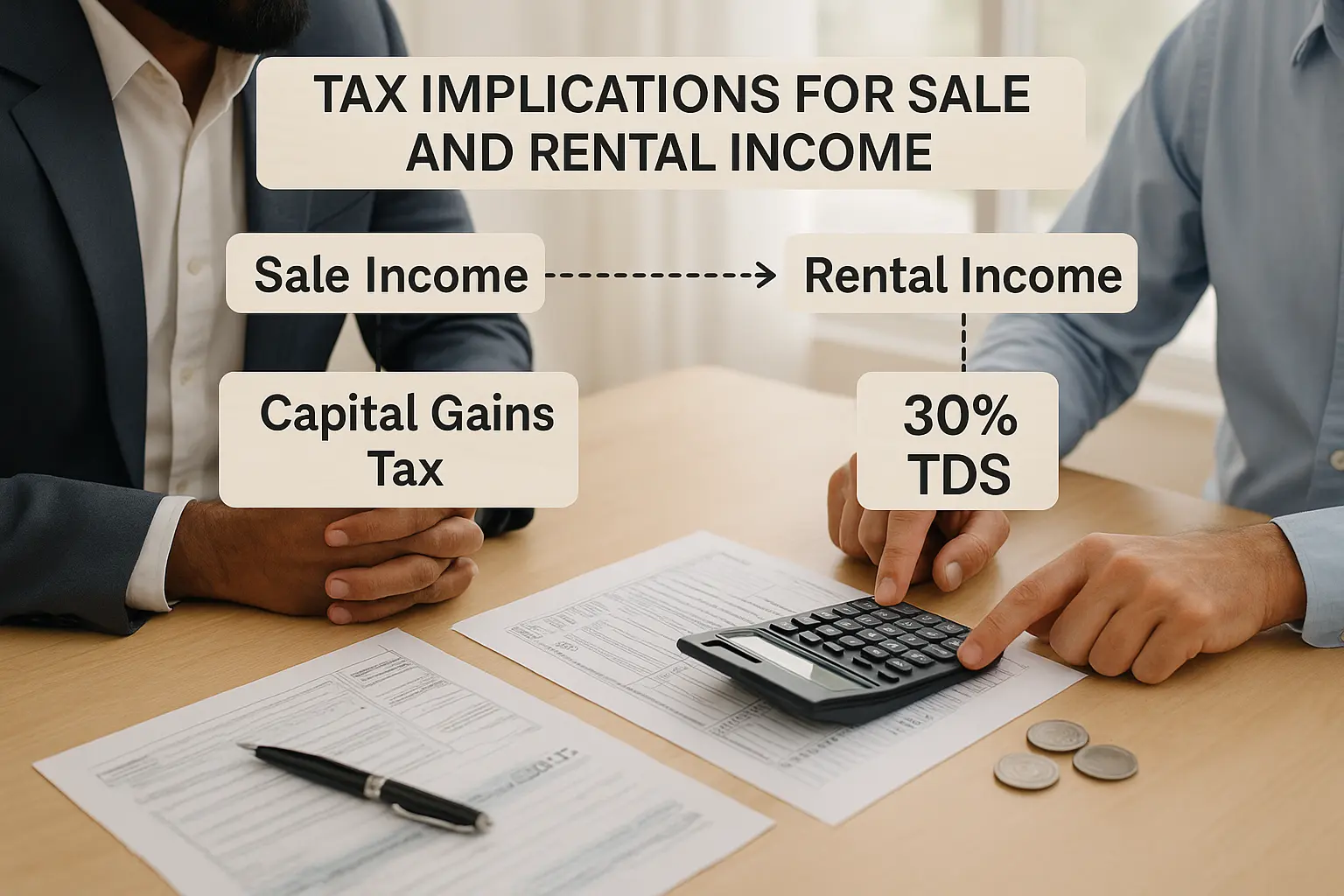

Tax Implications for Sale and Rental Income

Whether you’re selling your Indian property or renting it out, as an NRI, you are liable to pay applicable taxes under Indian law. Many NRIs overlook this step—only to face complications later while repatriating funds or during income tax scrutiny.

Let’s simplify the tax responsibilities in both scenarios:

1. Tax on Sale of Property

Capital Gains Tax:

-

Short-Term Capital Gains (STCG):

If the property is sold within 2 years of purchase, the profit is taxed as per your slab rate (usually 30% for NRIs). -

Long-Term Capital Gains (LTCG):

If held for more than 2 years, the gain is taxed at 20% with indexation benefits.

TDS Deduction:

-

The buyer must deduct TDS at:

-

20% on LTCG

-

Slab rate on STCG (usually 30%)

-

Plus applicable surcharge and cess

-

-

TDS is deducted on total sale value, not just gains, unless a lower/nil TDS certificate is obtained in advance from the Income Tax Department.

Tax Rebate:

You may save capital gains tax under Section 54 or 54EC if you reinvest in another property or NHAI/REC bonds, respectively.

2. Tax on Rental Income

-

Rental income earned in India is fully taxable in India, regardless of where you live.

-

Tenants must deduct 30% TDS and deposit it against your PAN.

-

You must file your income tax return in India to declare rental income and claim deductions under Section 24 (standard 30% deduction + home loan interest).

Double Taxation Relief

If your resident country has a Double Taxation Avoidance Agreement (DTAA) with India (like USA, UK, Canada, UAE), you can:

-

Avoid paying tax twice on the same income

-

Claim credit in your home country for the tax paid in India

Role of Power of Attorney (PoA) for NRIs

Managing property in India from thousands of miles away can be challenging. This is where a Power of Attorney (PoA) becomes an essential legal tool for NRIs. It allows a trusted individual in India to act on your behalf for property-related activities like selling, renting, registering documents, and handling banking formalities.

What Is a Power of Attorney?

A Power of Attorney is a legal authorization that grants someone (usually a relative, lawyer, or property manager) the right to represent you in legal and financial matters concerning your Indian property.

There are two main types:

-

General PoA – Covers a wide range of actions including buying, selling, leasing, managing, and collecting rent.

-

Special PoA – Limited to a specific transaction (e.g., registering a sale deed or collecting rental income).

How Can NRIs Create a Valid PoA?

-

Draft the PoA clearly stating the scope, rights, and limitations.

-

Get it notarized in the country where you’re residing.

-

Attest it at the Indian Consulate/Embassy in your foreign country.

-

Send it to India, where it must be adjudicated (stamped) at the local registrar office in the state where the property is located.

Only after this process is complete, the PoA becomes valid for legal use in India.

What Can a PoA Holder Do?

-

Sign property sale deeds

-

Register rent agreements

-

Receive payments on your behalf

-

Represent you before authorities and sub-registrars

-

Submit TDS, PAN, and tax forms

Note: The PoA holder cannot repatriate funds abroad unless authorized by a special clause.

Caution for NRIs:

-

Choose someone you completely trust.

-

Always limit the validity and scope to prevent misuse.

-

Avoid using outdated or generic PoA formats—get it professionally drafted.